Home-related loans at the five major banks increased by over 8 trillion won this year, but 12 trillion won of that came from policy loans like ‘DiDDimDol’ (mortgage loans) and ‘BeotimMok’ (jeonse loans). This means the banks’ own home-related loans actually decreased by about 4 trillion won. Financial authorities’ aggressive household loan management has led banks to keep mortgage rates high, analysts say. Those who don’t qualify for policy loans aimed at low-income groups have no choice but to take high-interest loans, fueling complaints. Voices are calling for changes to the current policy that solely blames banks for household loan growth.

Key Statistics

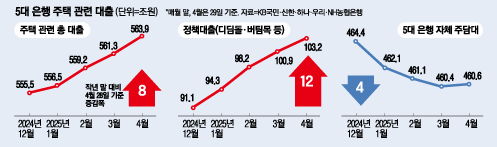

As of April 29, total home loans at KB Kookmin, Shinhan, Hana, Woori, and NH NongHyup banks rose from 555.5 trillion won (Dec 2024) to 563.9 trillion won, up 8.3 trillion won. However, policy loans grew by 12.1 trillion won during the same period, while commercial loans fell by 3.8 trillion won.

Policy Loan Breakdown:

| Loan Type | Increase (KRW) | Details |

|---|---|---|

| DiDDimDol (Mortgage) | 8.4 trillion | Income ≤60M, house ≤500M, up to 250M at 2-3% |

| BeotimMok (Jeonse) | 3.7 trillion | Low-income renters |

Policy Loan Expansion

DiDDimDol criteria relaxed since 2023: Newlywed income limit raised from 70M to 85M combined (Oct 2023), newborn loan from 130M to 200M (Dec 2024). These low-rate loans (vs. commercial rates) drove growth despite regulatory pressure on banks.

Bank Challenges & Responses

Financial authorities maintain strict DSR (Debt Service Ratio) rules, with Stage 3 enforcement in July tightening loan limits further. Banks can’t pass on recent base rate cuts due to scrutiny. Shinhan Bank responds by easing jeonse loan risk controls outside Seoul (owner change allowed) and cutting ‘Shinhan Jeonse Loan’ rates by 0.2%p from Dec 2.

Industry Implications

Banks view ongoing commercial loan decline as serious, potentially impacting next year’s performance. With policy loans carrying the growth, calls grow to ease pressure on banks while maintaining prudent lending.”